Larry Finks 2018 Letter to CEOs is titled “Sense of Purpose” he writes:

“We also see many governments failing to prepare for the future, on issues ranging from retirement and infrastructure to automation and worker retraining. As a result, society increasingly is turning to the private sector and asking that companies respond to broader societal challenges. Indeed, the public expectations of your company have never been greater. Society is demanding that companies, both public and private, serve a social purpose. To prosper over time, every company must not only deliver financial performance, but also show how it makes a positive contribution to society. Companies must benefit all of their stakeholders, including shareholders, employees, customers, and the communities in which they operate.

Without a sense of purpose, no company, either public or private, can achieve its full potential. It will ultimately lose the license to operate from key stakeholders. It will succumb to short-term pressures to distribute earnings, and, in the process, sacrifice investments in employee development, innovation, and capital expenditures that are necessary for long-term growth. It will remain exposed to activist campaigns that articulate a clearer goal, even if that goal serves only the shortest and narrowest of objectives. And ultimately, that company will provide subpar returns to the investors who depend on it to finance their retirement, home purchases, or higher education.”

My personal view is that reflects close to a consensus view amongst thoughtful long-term investors and those interested or practicing a sustainable or integrated ESG part of their investment process.

However, I do not believe that this is the predominant line of investment practice in the assessment management world. I have no direct data on this, it’s culled from experience and anecdote. The reasons are multi-factorial compounded by incentive structures, short-term pressures and job career risk. A lot of what it means to be human is not initially geared for long-term sustainable thinking. Perhaps this will be humanity’s

downfall.

Under: A new model for corporate governance, Fink suggests: “ In managing our index funds, however, BlackRock cannot express its disapproval by selling the company’s securities as long as that company remains in the relevant index. As a result, our responsibility to engage and vote is more important than ever. “

“…The time has come for a new model of shareholder engagement … companies have been too focused on quarterly results; similarly, shareholder engagement has been too focused on annual meetings and proxy votes. If engagement is to be meaningful and productive – if we collectively are going to focus on benefitting shareholders instead of wasting time and money in proxy fights – then engagement needs to be a year-round conversation about improving long-term value.

“….: a company’s ability to manage environmental, social, and governance matters demonstrates the leadership and good governance that is so essential to sustainable growth, which is why we are increasingly integrating these issues into our investment process.

Companies must ask themselves: What role do we play in the community? How are we managing our impact on the environment? Are we working to create a diverse workforce? Are we adapting to technological change? Are we providing the retraining and opportunities that our employees and our business will need to adjust to an increasingly automated world?”

FT’s Authers comments: “CEOs who think this is politically correct claptrap (there must be plenty) can of course ignore him. They can be safe in the knowledge BlackRock is not going to sell, whatever happens”

(Truly active) managers oft scoff at passive managers ability to engage. 40 ppl engaging 4,000+ companies, is not 10 ppl engaging with 50 cos.

Passive managers remain skeptical of how many active portfolio managers are effectively engaging.

But as Dimson et al. Active Ownership academic study implies +ve stewardship is good for multiple stakeholders: employees, company, shareholders environment…

Long-term stewardship should be a win-win for All.

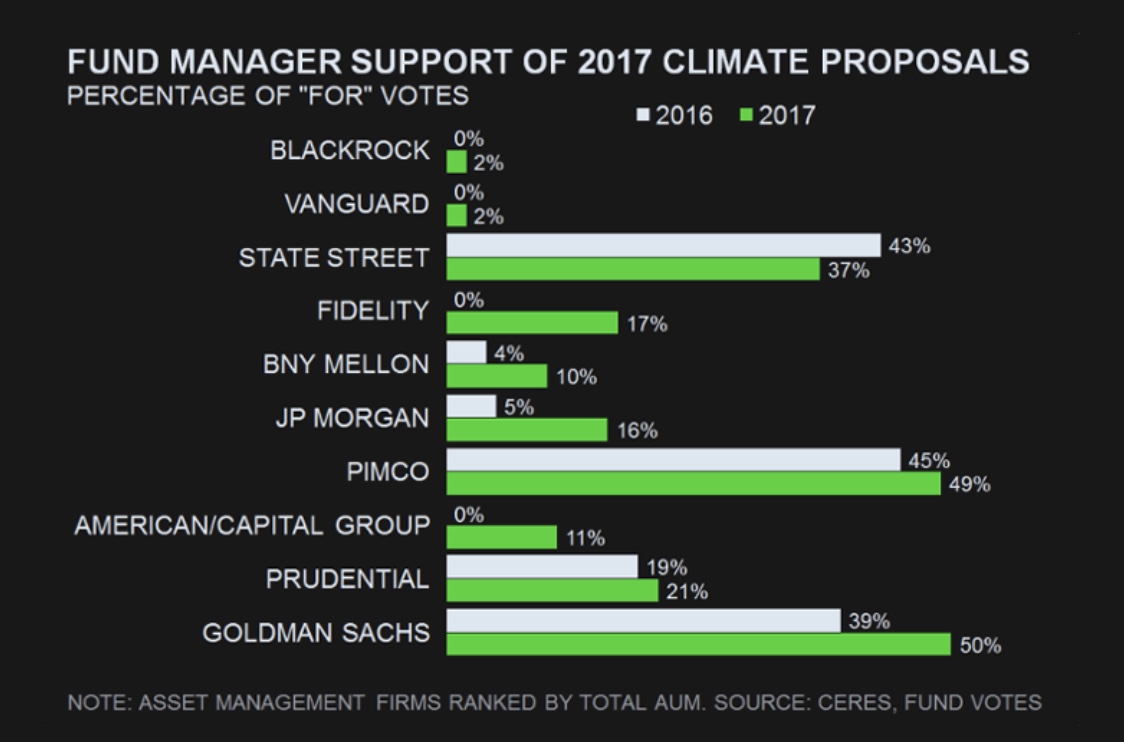

But as my earlier post on actual effectiveness and mainstreaming sustainability, where we can see Blackrock itself only voted in favour of Climate Change proposals for the first time in 2017 and then on very few (2%) of climate proposals, one could argue we still have some way to go.

There are also reasonable arguments that can be made suggesting that this is so far rhetoric which might not be supported by the current voting record. Although others would note it is complicated and that much good engagement can happen regardless of vote.

Link to climate proposals post

Link to BlackRock CEO 2018 Letter

Link to Active Ownership paper here: H/T Xi Li, Elroy Dimson and Oğuzhan Karakaş https://www.thendobetter.com/investing/2017/10/16/active-ownership-academic-study