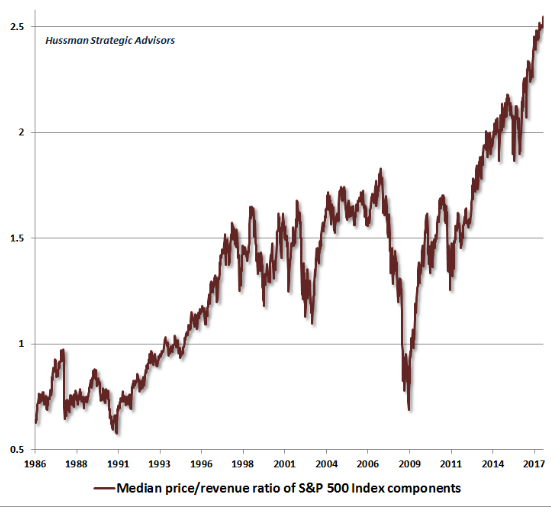

"Last week, the median price/revenue ratio of S&P 500 component stocks reached the highest level in history, advancing far beyond the levels reached at both the 2000 and 2007 market peaks." Writes John Hussman (See chart above and on his site).

Hussman, along with Albert Edwards (currently at SocGen (with Andrew Lapthorne, his recent chart here), I worked with him at Dresdner Kleinwort) and to some extent James Montier (who also worked alongside Albert at DK previously, but has a behavioural economist streak to his work; now at GMO) and Jeremy Grantham (at GMO) have tended to put quite some weight on these type of metrics and valuation discipline, at least for long cycle returns (around 7 years). It's interesting that most of this group are chiming quite loudly, with the possible exception of Grantham who is ringing in a slightly different key (suggesting much slower reversions to the mean than before). The world of macro has so many cross currents (I shall try and put forward the optimists view in later posts). One reason I prefer micro - bottom up company fundamentals.

There is another interesting chime with Nassim Taleb's thinking from his pop risk books. This idea that we do not handle "fat tails" or "Black Swan" events very well. That models do not account for these events well (real world is not "normal" or "gaussian"). This dovetails well with Hyman Minsky's observation/theory on why we have and will always have boom/bust cycles.

What to do about this ? That's an even longer more complex answer. I would suggest it pays to be prepared (Warren Buffet always seems to be), but if you can't perhaps don't make life plans based on what we've seen in the last 5 years, but leave enough flex for a plan B.

I leave you with another Hussman chart on his view that markets are over valued (for long term performance) on many (reliable) metrics.

Cross fertilise. Read about the autistic mind here and ideas on the arts here.