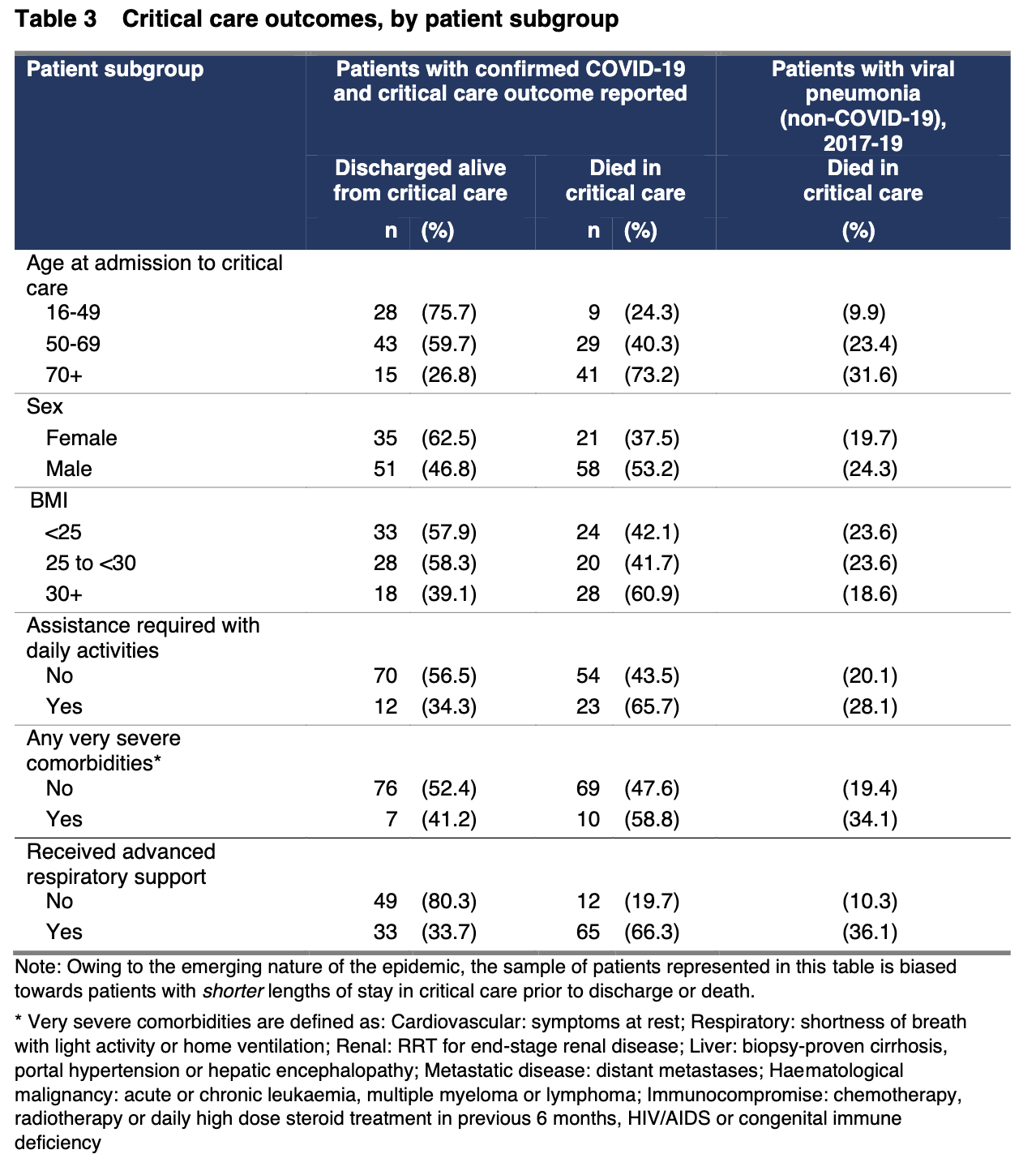

Short update on COVID vaccine timelines. US/EU timelines have slipped by 1 -3 months, but China has held up since my August estimates. Treat all estimates with caution etc.

I thought I would update on my speculative COVID vaccine thoughts given the moving timelines here. There are >100 vaccine projects and COVID treatments in motion, and although recent vaccine timelines have slipped, it looks ;like we will have a vaccine at some point. When? is a key debate. Given the challenges around public health interventions, (lockdowns etc.) in EU/NA - one way we can cut the knot is to go fast on the vaccine. This is one reason why (althoguh not without some downsides) I support the UK challenge trials starting in early 2021. That said we have some decent chances of vaccines by very late this year / Jan 2021. Below is a moderatel positive scenario of how the US could be vaccinated in 2021.

Oct 2020, estimates. Treat with caution.

I think China will have a vaccine starting to distribute to the public by Dec 2020. Chinese officials have indicated data is positive and they are willing to approve.

The UK has an 80% chance (IMO) of a vaccine in Dec/Jan for at risk populations (AZ/Oxford, timelines, newspaper leaks) under emergency approval. The early data is promising and despite the delays, if there were serious safety issues I would have expected to have had more negative news here.

The US has a chance for an emergency vaccine approval late Dec (slipping) or Jan, there are two shots on goal here (Moderna and Pfizer), and I rate the chances around the 70% level (although 40% and dropping for before year end as both have slipped, but still at 70% or so in Q1 2021 time frame). (This is down slightly from earlier due to challenges in the trials). Again early data is promising and no catastrophic safety events seen. Full approvals are more debatable than emergency (as hurdles different, but mixed messages from FDA makes this uncertain). The AZ trial stalled for longer in the US, so is more likely a Q1 2021 event as US don’t seem to want to recognize the UK/EU regulators view here.

Antibody treatments (Regeneron/Roche, Lilly) have a 90% chance of emergency approval before year end, but are only available in limited doses of around 5m to 10m doses pa. Data has been positive especially in the mild-moderate pateients.

12 Oct, 2020 Source: Gallup for Sep survey.

There are a lot of variations on scenarios here, and supply and distribution as well as anti-vax movements are all other factors to consider. Some polls but vaccine willingness only at or so 50% in the US. Debates arise are on (1) Willingness to vaccinate (2) Regulatory caution around durability as well as efficacy (3) social-political pressures.

It is of note that China is more advanced here seemingly than NA/EU and generally the countries outside of EU/NA are potentially faring better.

15 Leading vaccine projects, Source: Milken, press releases